6 Key Difference Between Coin And Token With Examples

July 26, 2023Top 25 Remote Bookkeepers & Accountants To Hire in 2025

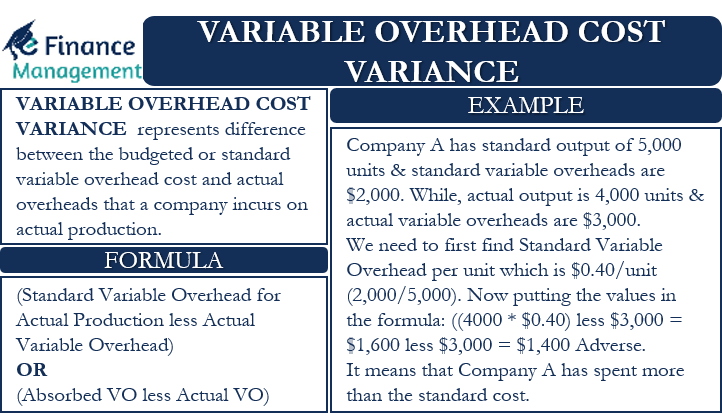

September 1, 2023

Let’s assume it is December 2022 and DenimWorks is developing the standard fixed manufacturing overhead rate for use in 2023. As mentioned above, we will assign the fixed manufacturing overhead on the basis of direct labor hours. Fixed overhead budget variance is favorable when actual fixed overhead incurred are less than the budgeted amount and it is unfavorable when the actual fixed overheads exceed the budgeted amount. In other words, FOH budget variance is the amount by which the total fixed overhead calculated as per the fixed overhead application rate exceeds or falls short of the actual total fixed overhead cost incurred for the period. In this example, the fixed overhead budget variance is positive (2,000 favorable), and the fixed overhead volume variance is negative (-1,040 unfavorable), resulting in an overall positive overhead variance (960 favorable).

Overhead Variances FAQs

- The fixed overhead production volume variance is favorablebecause the company produced and sold more units thananticipated.

- Thus budgeted fixed overhead costs of $140,280shown in Figure 10.12 will remain the same even though Jerry’sactually produced 210,000 units instead of the master budgetexpectation of 200,400 units.

- The fixed overhead volume variance is also one of the main standard costing variances, and is the difference between the standard fixed overhead allocated to production and the budgeted fixed overhead.

This variance would be posted as a debit to the fixed overhead volume variance account. A favorable fixed overhead spending variance arises when the actual fixed overheads incurred by the company are lower than the budgeted fixed overheads. The company can calculate fixed overhead volume variance with the formula of standard fixed overhead applied to actual production deducting the budgeted fixed overhead. Suppose a company uses a standard absorption rate of $ 15 per unit, for an estimated production of 1,500 units. If the production output is exactly the same as planned with no abnormal fixed overhead changes then there will be no fixed overhead variances.

Formulas to Calculate Overhead Variances

It is likely that the amounts determined for standard overhead costs will differ from what actually occurs. To operate a standard costing system and allocate fixed overhead, the business must first decide on the basis of allocation. Various methods can be used to allocate the fixed overhead including for example, the number of direct labor hours used in production or the number of machine hours used. The method of allocation is more fully discussed in our applied overhead tutorial. Fixed overhead budget variance is one of the two main components of total fixed overhead variance, the other being fixed overhead volume variance. Favorable fixed overhead expenditure variance suggests that actual fixed costs incurred during the period have been lower than budgeted cost.

Formula:

Since the expenditure is considered to be under the control of management, the overhead budget variance is referred to as a controllable variance. Volume variance is further sub-divided into efficiency variance and capacity variance. After the reasons have been highlighted the company takes measures to deal with any material variances throughout the year to minimize costs. In such a case, the company incurs an entirely new expense that the production department didn’t anticipate. This variance arises due to the difference in the number of working days when the actual number of working days is greater than standard working days. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

Calculating the Fixed Overhead Expenditure Variance

The figure in hours here can either be labor hours or machine hours depending on which one is more suitable for the measurement in the production. By analysing variances a business is able to quickly see how well it is performing in terms of meeting budget expectations. If considerable differences are noted within fixed overhead expenditure the fixed overhead spending variance is calculated as: it is worth investigating why this is the case. Fixed overheads do not tend to change unexpectedly so if there has been an increase in spending in this area a business needs to find out the reason as soon as possible. For example, a non-cash item such as depreciation calculations depend on the costing method adopted by the management.

Do you already work with a financial advisor?

He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. If the balances are considered insignificant in relation to the size of the business, then they can simply be transferred to the cost of goods sold account. Motors PLC is a manufacturing company specializing in the production of automobiles.

In case of fixed overhead, the budgeted and flexible budget figures are exactly the same. For example, the production department of Tahkila Industrials expects that the annual fixed overheads of the company will be $500,000 for the year ended 2019. At the start of a period XYZ Limited estimates that they will incur £30,000 of fixed overheads.By the end of the period they had actually spent £28,000 on fixed overheads.

We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

The other variance computes whether or not actual production was above or below the expected production level. To determine the overhead standard cost, companies prepare a flexible budget that gives estimated revenues and costs at varying levels of production. The standard overhead cost is usually expressed as the sum of its component parts, fixed and variable costs per unit. Note that at different levels of production, total fixed costs are the same, so the standard fixed cost per unit will change for each production level. However, the variable standard cost per unit is the same per unit for each level of production, but the total variable costs will change. Recall that the standard cost of a product includes not only materials and labor but also variable and fixed overhead.